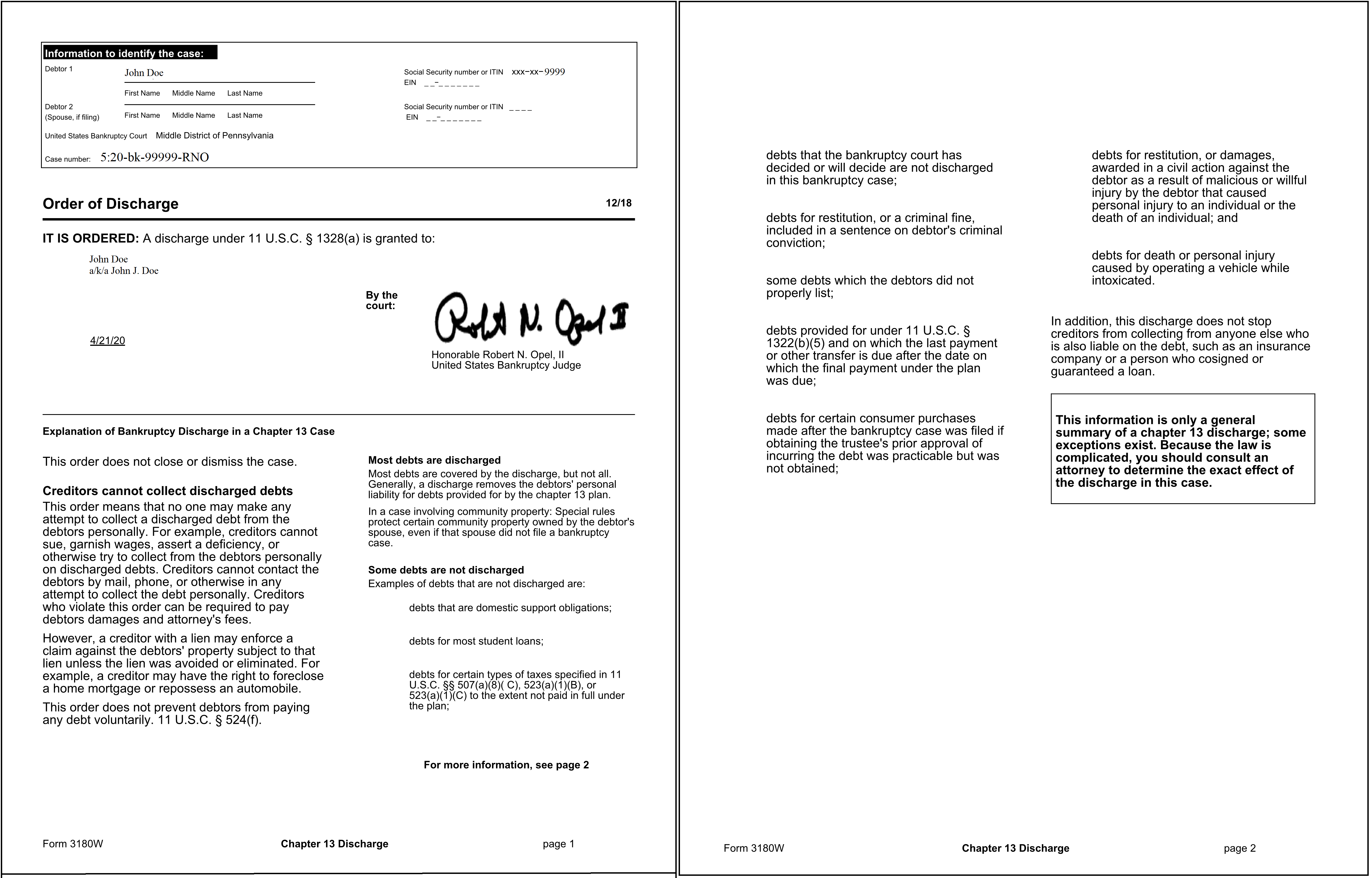

There are numerous alternatives readily available for investing. These are normally subject to your earnings, non reusable cash, and long-lasting goals. While conserving for retirement, a 2nd residential or commercial property financial investment, or otherwise can be a great goal, you may desire to talk with a monetary consultant about how to use your cash most advantageously.

House owners who wish to slash off dollars from their regular monthly home mortgage payment as well as save money on interest, may think about a home loan recast. A mortgage recasting, or loan recast, is when a borrower makes a large, lump-sum payment towards the primary balance of their home mortgage and the lender, in turn, reamortizes the loan.

Recasting cuts your month-to-month payments and the quantity of interest you'll pay over the life of the loan. It does not, however, affect your rates of interest or the regards to your loan. In this way, home mortgage modifying deals 2 and possibly 3 appealing advantages for property owners with some extra money in their pocket to pay for the balance: Lower regular monthly payments.

If you have a low rate of interest, that will remain the very same. (Conversely, if your rate of interest is high, recasting won't help that.) In order to do a loan recast, customers should make a big lump-sum payment towards the loan principal. Lenders generally require $5,000 or more to modify a mortgage.

There are typically fees connected with recasting. The fees vary by loan provider; however they normally do not go beyond a few hundred dollars. Recasting not just leads to lower regular monthly payments however borrowers will also pay less interest over the life of the loan. For example, if your 30-year mortgage carries a principal balance of $200,000 with a 5 percent interest rate, you might pay $1,200 monthly.

The 6-Minute Rule for In What Instances Is There A Million Dollar Deduction Oon Reverse Mortgages

Of course, the cash you sink into the house in the recast won't be offered for investing or other purposes. Remember, recasting doesn't lower the term of your home loan, simply how much you pay every month. Utilize our amortization schedule calculator to determine what your brand-new monthly payments will be.

It's also not something that's generally marketed, but many of the big banks offer can a timeshare contract be cancelled it, including Chase, Bank of America and Wells Fargo. Plus, not all home mortgages get approved for recasting; some kinds of loans, like FHA loans and VA loans, can't be modified. There's a huge difference between modifying a home mortgage and re-financing one, despite the fact that both can assist borrowers conserve cash.

With recasting, you're keeping your existing loan, just adjusting the amortization. what banks give mortgages without tax returns. You wouldn't have the ability to get a lower rates of interest with recasting, like you might with refinancing. On the other hand, if your rates of interest is currently low then re-financing might have a negative effect especially if the existing rates are greater.

The new loan would pay off your existing loan, so you might end up with a brand-new home loan as well as brand-new rates of interest. People generally do this to get a lower interest rate or to go from an adjustable-rate mortgage to a fixed-rate mortgage. If you currently have a fixed-rate home loan with a low interest rate, then a refi would not help you.

Recasting has some appeal since it's relatively simple to do and it's a relatively economical way to decrease regular monthly payments if you have the cash. Here are a couple of factors you might desire to think about recasting your existing home mortgage: Lower your month-to-month payments by making one swelling amount. Avoid needing to requalify for a brand-new loan.

The Facts About What Is A Bridge Loan As Far As Mortgages Are Concerned Revealed

The greatest monetary downside of recasting is that you're putting a large amount of cash david lamberth into equity. These are a few reasons you may desire to reassess recasting: It does not shorten the length of your home loan. Your interest rate stays the same, a downside if you have a greater interest rate.

Lender charges a cost, generally no more than a few hundred dollars, to modify a loan. In the current climate, with fairly low mortgage rates and a strong market, a loan recast may not make sense for some.

Home loan recasting is one method to decrease your regular monthly home loan payments. It's less common than refinancing or modifying a loan, and it's hardly ever promoted, however it decreases home loan payments for those who can apply a swelling amount towards their loan's principal. When you modify your home mortgage, you pay your loan provider a big amount towards your principal, and your loan is then reamortized to put it simply, recalculated based upon your new, lower balance.

It's a relocate to make if you desire to minimize your interest cost without reducing your loan term, says Eric Gotsch, a sales supervisor for Wells Fargo Home Home Mortgage (what lenders give mortgages after bankruptcy). The most typical factor for recasting is if you've purchased a home but not yet offered your previous one, says Jim Hettinger, executive vice president of operations at Surefire Rate, an online home loan lender.

Modifying is also ideal for people who get a big sum of cash and desire to lower their mortgage expenditures, Gotsch says. This typically occurs when somebody gets an inheritance, an investment distribution or a large bonus offer, or has a nontraditional earnings stream, he states. In many cases, you'll need a minimum of $5,000 to modify your home loan.

how much is a time share >An Unbiased View of What Is A Non Recourse State For Mortgages

When you refinance, you get a brand-new loan, with various terms, to replace the old one. You could get a lower rates of interest or switch from an adjustable to a fixed rate or from 15 years to thirty years, for example. The benefit of a home loan recast is basic: It reduces your month-to-month payments, making your housing costs more cost effective.

You will not need a credit check or an appraisal to modify, making it an easier choice than refinancing. There's a great chance that it will be cheaper than refinancing, too, given that you will not face the normal array of closing expenses. Nevertheless, you might need a history of on-time payments to recast.

Loans purchased by Fannie Mae and Freddie Mac can be modified, he says, however Federal Housing Administration and Veterans Affairs loans can't. Furthermore, jumbo or nonconforming mortgages might be eligible for recasting just on a case-by-case basis, Hettinger states. Some lending institutions charge a fee for the service, normally a couple of hundred dollars, so inquire about the expense.

" There are likewise differing policies concerning how much a customer will have to put down to modify the loan," Hettinger says. "Make sure you have your loan officer talk to the servicer before entering into a closing assuming you can modify a couple of months down the line." Lenders who offer recasting typically don't promote it.

We will never disclose or sell your email address or any of your information from this website. We do extremely welcome posts and neighborhood interaction, and registering is just part of the posting system. Financial Samurai exists to believed provoke and gain from the neighborhood. Your decisions are yours alone and we remain in no way responsible for your actions.